Many founders discover this only after they've already begun exploring an IPO, which creates costly delays. A Private Limited Company, regardless of its revenue or growth trajectory, cannot invite the public to subscribe to its shares. Full stop.

This article covers which types of companies can legally issue shares to the public, the two primary listing routes available to qualifying companies, the eligibility conditions they must meet under SEBI's ICDR Regulations, and the mistakes founders make before attempting to go public.

Key Takeaways

- Only Public Limited Companies can issue shares to the public — Private Limited Companies are prohibited under Section 2(68) of the Companies Act, 2013

- Two listing routes exist: the Main Board (NSE/BSE) for larger companies and the SME Exchange (NSE Emerge/BSE SME) for smaller, growing ones

- Already-listed companies have separate capital-raising routes — FPOs, Rights Issues, and QIPs — distinct from an initial public offering

- SEBI's ICDR Regulations, 2018 set the eligibility criteria every company must clear before listing — from financials to governance to free float

- A Private Limited Company must formally convert to a Public Limited Company before pursuing any public listing

What Does "Issuing Shares to the Public" Mean in India?

Issuing shares to the public is the formal process through which a company offers ownership stakes to the general population of investors — not a select group of private individuals. Once issued publicly, these shares are listed and traded on a recognised stock exchange under SEBI oversight.

The legal distinction matters. Under Section 40 of the Companies Act, 2013, every company making a public offer must apply to one or more recognised stock exchanges before the offer is made — meaning listing is not optional after a public issue, it is mandatory.

This is distinct from:

- Private placements — offered to identified persons under Section 42 of the Companies Act, 2013

- Rights issues — restricted to existing shareholders

- Bonus issues — no fresh capital is raised

Public capital delivers real advantages for companies ready to take this step:

- Raises large sums from a broad investor base rather than a handful of backers

- Creates a market-determined valuation that strengthens negotiating position

- Improves brand credibility with customers, suppliers, and future hires

- Provides liquidity for existing shareholders who have waited years to exit

These benefits come with ongoing obligations — audited disclosures, board governance standards, and continuous SEBI compliance — that require genuine preparation well before the process begins.

Which Types of Companies Can Issue Shares to the Public in India?

The answer is clear: only Public Limited Companies can issue shares to the general public in India, and only after fulfilling SEBI's conditions and obtaining regulatory clearances.

Section 2(68) of the Companies Act, 2013 defines a private company as one whose articles prohibit any invitation to the public to subscribe for its securities. Section 23 reinforces this: private companies may only issue securities by rights issue, bonus issue, or private placement — not by public offer.

A Private Limited Company must convert to a Public Limited Company before it can pursue a public listing. Among qualifying public companies, the right route depends on the company's size, revenue stage, and capital requirements.

Three categories of companies can issue shares to the public:

Public Limited Companies Listed on the Main Board (NSE/BSE)

The Main Board is the primary route for larger, established companies seeking to raise capital from the broadest investor base in India. The process involves filing a Draft Red Herring Prospectus (DRHP) with SEBI, obtaining regulatory clearances, completing bookbuilding for price discovery, and listing on NSE or BSE.

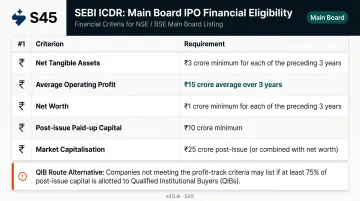

SEBI ICDR financial thresholds for Main Board eligibility (per SEBI's May 2025 ICDR FAQs):

| Criterion | Requirement |

|---|---|

| Net Tangible Assets | ₹3 crore minimum in each of the preceding 3 years |

| Average Operating Profit | ₹15 crore average over preceding 3 years (with profit in each year) |

| Net Worth | ₹1 crore minimum in each of the preceding 3 years |

| Post-issue Paid-up Capital | Not less than ₹10 crore (per NSE) |

| Market Capitalisation | Not less than ₹25 crore (post-issue) |

Companies that don't meet the profitability route criteria may still qualify through the QIB Route, provided at least 75% of the net offer is allotted to Qualified Institutional Buyers.

Main Board listings suit companies with consistent revenue growth, multi-year financial fundamentals, and large capital requirements. The costs reflect that scale: higher compliance spend, longer timelines from DRHP filing to listing, and a substantially heavier disclosure burden once public.

Public Limited Companies Listed on the SME Exchange (NSE Emerge/BSE SME)

The SME Exchange was created to give smaller, high-growth Public Limited Companies access to public capital without the demanding thresholds of the Main Board. On this platform, companies file their offer documents with the Stock Exchange rather than directly with SEBI.

Key eligibility criteria (per NSE Emerge and BSE SME current guidelines):

- Post-issue paid-up capital ceiling: Must not exceed ₹25 crore (both NSE Emerge and BSE SME)

- Operating profit: EBITDA of at least ₹1 crore for 2 out of 3 preceding financial years

- Track record: Minimum 3-year operating history required

- Net worth (BSE SME): At least ₹1 crore for 2 preceding full financial years

- Leverage (BSE SME): Leverage ratio must not exceed 3:1

This route suits growing businesses in manufacturing, services, or technology with real revenue and a demonstrated operating history — those using an SME listing as a stepping stone toward eventual Main Board migration.

Compared to a Main Board IPO, the trade-offs look like this:

- Lower cost and faster execution — fewer regulatory touchpoints and a lighter prospectus process

- Smaller institutional base — secondary market liquidity is thinner, which affects price discovery and post-listing trading volumes

Already-Listed Public Companies Doing Secondary Offerings

The third category covers Public Limited Companies already listed on a stock exchange that wish to issue additional shares through secondary mechanisms:

- Follow-on Public Offerings (FPO) — a further public offer by a listed issuer

- Rights Issues — offered to existing shareholders at a defined price

- Qualified Institutional Placements (QIP) — allows listed companies to raise capital quickly from institutional buyers without a full public offer process

These mechanisms are governed under Chapters III, IV, and VI of the SEBI ICDR Regulations, 2018 respectively.

With a public shareholder base in place, secondary issuance is typically faster and less expensive than an IPO. That said, each mechanism still requires SEBI compliance, board and shareholder approvals, and careful dilution management. These routes remain available only to listed companies in good regulatory standing.

Eligibility Conditions a Company Must Meet to Issue Shares to the Public

Legal Structure Requirement

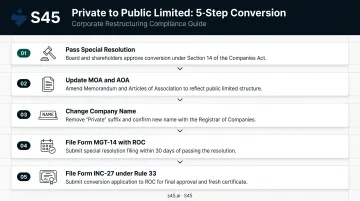

The company must be structured as a Public Limited Company with a valid Certificate of Incorporation under the Companies Act, 2013. If the company is currently a Private Limited Company, it must go through a formal conversion process:

- Pass a special resolution by shareholders (Section 14, Companies Act, 2013)

- Update the Memorandum and Articles of Association to remove private company restrictions

- Change the company name to remove "Private"

- File Form MGT-14 with the Registrar of Companies within 30 days of the resolution

- File Form INC-27 for the conversion under Rule 33 of the Companies (Incorporation) Rules, 2014

Mandatory Intermediary Appointments

To issue shares publicly, a company must appoint SEBI-registered intermediaries including:

- Book Running Lead Manager (BRLM/Merchant Banker) — responsible for due diligence, DRHP preparation, and managing the bookbuilding process. The lead manager must submit a due diligence certificate to SEBI at least 2 weeks before issue opening

- Registrar to the issue — must be registered with SEBI and have connectivity with all depositories (NSDL and CDSL)

The quality of this team matters. The merchant banker's due diligence is thorough by design — it will surface every governance gap, related-party transaction, and disclosure inconsistency in the company's records.

S45, working with Narnolia as Category-I SEBI-Registered Merchant Banker, runs a pre-filing readiness assessment that surfaces documentation and compliance gaps before formal SEBI review begins — so the DRHP that reaches the regulator is clean from the start.

Governance and Disclosure Readiness

Companies must have:

- Audited financial statements covering the required track record period

- Clean promoter background — no regulatory disqualifications

- Restated financials prepared in accordance with applicable accounting standards

- Functioning board with independent directors meeting SEBI requirements

- No unresolved related-party transaction issues that would raise SEBI concerns

Each of these requirements sounds straightforward until you're in a data room at 11pm restating three years of financials. Companies consistently underestimate how long it takes to bring governance and financial records to a standard that holds up under public scrutiny. Main Board candidates typically spend 12–18 months on readiness work before filing — not because the rules are unclear, but because the records rarely are.

Common Mistakes to Avoid When Preparing to Issue Shares to the Public

Attempting to List Without the Right Structure or Route

The most fundamental mistake: initiating IPO preparations while still structured as a Private Limited Company, or choosing the wrong exchange for the company's actual financial profile. Selecting the Main Board when the SME Exchange is more appropriate (or vice versa) wastes months of management bandwidth, advisory fees, and preparation effort.

Route selection should be based on float analysis, offering structure, and realistic demand modelling — not on ambition or what the company aspires to be.

Underestimating Documentation and Governance Readiness

Companies that enter the IPO process with unresolved issues routinely face months of delays — or abandon the process entirely. SEBI's review and the merchant banker's due diligence exist to catch exactly these problems:

- Incomplete or restated financial records

- Unresolved related-party transactions

- Inadequate board independence or governance structure

- Disclosure gaps that trigger SEBI observations

Catching these issues early is far less expensive than correcting them mid-DRHP. S45's Readiness Scan covers board independence, financial track record, disclosure gaps, and ICDR eligibility — giving founders a clear picture of what needs fixing before the formal process begins.

Confusing Legal Eligibility With Market Readiness

Meeting SEBI's financial thresholds gets a company through the door — it does not guarantee investors will show up. Pricing discipline, a coherent investor story, and institutional-quality disclosures from day one are what determine whether a listing creates lasting value.

Founders who treat the IPO as purely a compliance exercise often face weak subscription and poor post-listing performance. The companies that list well treat it as a capital markets transaction from the first day of preparation — not from the day SEBI clears the DRHP.

Frequently Asked Questions

What kind of company can sell shares to the public?

In India, only Public Limited Companies that have received SEBI clearance and fulfilled the prescribed eligibility conditions under the ICDR Regulations can sell shares to the public. Private Limited Companies are legally prohibited from doing so under the Companies Act, 2013.

Can a private limited company issue shares to the public in India?

No. A Private Limited Company cannot invite the public to subscribe to its shares under Section 2(68) of the Companies Act, 2013. It must first convert to a Public Limited Company and then comply with all SEBI requirements before a public offering becomes possible.

What is the difference between a Main Board IPO and an SME IPO in India?

A Main Board IPO is for larger, more established companies listing on NSE or BSE with higher financial thresholds and SEBI review of the offer document. An SME IPO is for smaller companies listing on NSE Emerge or BSE SME with lower capital requirements and exchange-level review of the offer document.

How does a private limited company convert to a public limited company in India?

The process starts with a special resolution by shareholders, followed by updating the Memorandum and Articles of Association to remove private company restrictions and dropping "Private" from the company name. The company then files Form MGT-14 and Form INC-27 with the Registrar of Companies under the Companies Act, 2013.

What are the SEBI eligibility criteria for a company to go public in India?

Under SEBI's ICDR Regulations, 2018, a company must meet minimum thresholds: post-issue paid-up capital of ₹10 crore, net tangible assets of ₹3 crore in each of the preceding 3 years, and average operating profit of ₹15 crore over 3 years. Appointment of SEBI-registered intermediaries — including a merchant banker — is also mandatory.

Can a company issue shares to the public without listing on a stock exchange in India?

Public share issuance in India requires listing on a SEBI-recognised stock exchange such as NSE or BSE. Any company raising capital from the general public must go through the formal IPO and listing process governed by SEBI regulations — there is no lawful alternative route for unlisted companies.