Key Takeaways

- QIBs — mutual funds, banks, insurers, FPIs — receive up to 50% of the net offer in a book-built IPO.

- Their central function is price discovery: large-ticket bids during bookbuilding anchor the final issue price within the price band.

- Anchor investors bid one day before the IPO opens; their allotment is locked 50% for 30 days, 50% for 90 days.

- High QIB oversubscription signals institutional conviction but does not guarantee post-listing performance.

- An unfilled QIB quota is a serious red flag — one that often precedes pricing revisions or IPO withdrawal.

What Is a QIB? Meaning and SEBI Definition

A Qualified Institutional Buyer (QIB) is a large institutional investor that SEBI formally recognises as having the financial expertise, capital depth, and risk assessment capability to participate in capital markets without the level of regulatory protection extended to retail investors.

The current governing definition appears in Regulation 2(1)(ss) of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018, notified as SEBI/LAD-NRO/GN/2018/31 on September 11, 2018. This regulation is the primary legal anchor for all QIB-related IPO rules — earlier frameworks, including the 2009 ICDR Regulations, established the category, but the 2018 regulation as last amended on March 21, 2026 governs current practice.

Not every institution qualifies as a QIB. SEBI mandates specific criteria across three dimensions:

- Entity type — only designated categories such as mutual funds, FPIs, insurance companies, and scheduled commercial banks are eligible

- Registration requirements — the institution must hold applicable SEBI or regulatory registrations

- Corpus thresholds — certain categories require minimum asset or corpus levels

This selectivity is what gives QIB participation its credibility as a market signal.

SEBI gives QIBs preferential allocation because their bookbuilding behaviour functions as market validation. A QIB's decision to bid at a particular price reflects institutional due diligence — financial modelling, sector analysis, management assessment — that retail investors cannot replicate on their own.

When a mutual fund or insurance company participates as a QIB, it is deploying capital on behalf of SIP investors, policyholders, and pension contributors. QIB participation is, in that sense, broadly representative of public savings — not just institutional balance sheets.

Who Qualifies as a QIB in India?

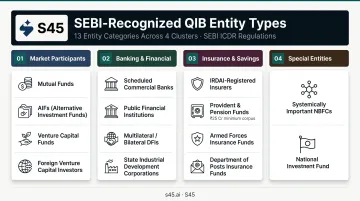

Entity Types Recognised Under SEBI ICDR 2018

Regulation 2(1)(ss) of the SEBI ICDR Regulations 2018 recognises the following entity types as QIBs:

- Mutual funds registered with SEBI

- Venture capital funds and alternative investment funds (AIFs)

- Foreign venture capital investors registered with SEBI

- Foreign portfolio investors — excluding individuals, corporate bodies, and family offices

- Scheduled commercial banks

- Public financial institutions

- Multilateral and bilateral development financial institutions

- State industrial development corporations

- Insurance companies registered with IRDAI

- Provident funds and pension funds with a minimum corpus of ₹25 crore

- The National Investment Fund

- Insurance funds managed by the armed forces or the Department of Posts

- Systemically important NBFCs

Key Thresholds and Exclusions

Two thresholds matter here:

- ₹25 crore minimum corpus applies to provident and pension funds — a smaller fund does not qualify, regardless of its institutional standing.

- Promoters, their relatives, and merchant bankers associated with the issue are explicitly excluded from the QIB category by SEBI.

How QIBs Differ from Retail and NII Investors

| Feature | QIBs | NIIs | Retail |

|---|---|---|---|

| Bid at cut-off price | ❌ Not permitted | ❌ Not permitted | ✅ Permitted |

| Bid withdrawal after IPO close | ❌ Not permitted | ❌ Not permitted | ❌ Not permitted after close; can revise during bid period |

| Allotment method | Proportionate | Draw of lots (post-2022 split) | Draw of lots |

| Advance payment | ASBA-led (check current GID) | ASBA-led | ASBA/UPI |

The no-withdrawal rule for QIBs after the IPO closes is significant — it reinforces their commitment to the issue and underpins the credibility of their bids.

The Role of QIBs in an IPO

Price Discovery

In a book-built IPO, the final issue price is not predetermined. It emerges from QIB bidding behaviour during the subscription period. When institutions submit large-ticket bids across the price band, investment bankers can identify where genuine demand is anchored and set the final price accordingly.

This is the most technically important function QIBs serve. Their bids carry information: the price at which a QIB bids signals their view of fair value. That is why SEBI reserves the largest allocation for them and why bookbuilding is structured around institutional participation first.

Credibility and Signalling

When well-known institutions — LIC, large domestic mutual funds, sovereign wealth funds, marquee FPIs — subscribe to an IPO, the effect on retail sentiment is disproportionate. Most retail investors cannot conduct independent due diligence on every issuer. QIB participation acts as a proxy signal: sophisticated capital evaluated this company and committed.

That signal is powerful. The quality of the institutional book matters as much as its size: a QIB register dominated by long-only funds carries different credibility than one driven by short-term arbitrageurs, even if the subscription multiple looks similar.

Capital Absorption and Scale

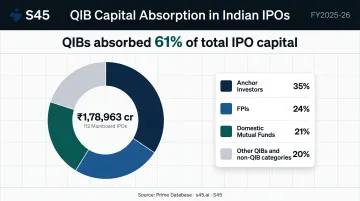

Prime Database data for FY2025-26 shows that across 112 mainboard IPOs raising ₹1,78,963 crore, QIBs including anchor investors absorbed 61% of the total IPO amount — with anchors accounting for 35%, FPIs 24%, and domestic mutual funds 21% of total IPO capital. This is not a marginal contribution; it is the structural backbone of how large IPOs get done.

Post-Listing Stability

QIBs managing mutual fund NAVs, insurance float, or pension obligations are not typically trading the IPO as a short-term position. That tendency (not a guarantee) contributes to price stability in the secondary market during the early weeks after listing.

The counterpoint: anchor lock-in expiry dates at 30 and 90 days create predictable supply windows. Business Standard reported that shares worth approximately $24 billion from 108 recently listed companies were set to become eligible for trading between December 2025 and March 2026. Lock-in expiry is an investor relations event, not an afterthought.

Issuers who treat lock-in expiry as a calendar date rather than a communication window often face avoidable secondary market pressure. Key dates to manage actively:

- Day 30: First anchor lock-in expiry; earliest window for short-term anchor exits

- Day 90: Full anchor lock-in release; largest potential supply event

- Ongoing: Institutional holding disclosures signal whether the long-only cohort is holding or rotating out

The Issuer-Side Dimension

For a company going public, attracting quality QIB participation is not just about meeting the regulatory quota. It builds a credible institutional register that supports long-term investor relations, research coverage, and secondary market liquidity. Investment banks with strong institutional relationships and disciplined bookbuilding processes play a direct role in achieving this.

S45 has generated over ₹1,83,000 crore in cumulative bids across 26 IPOs since July 2023, drawing on a mapped institutional network across QIB, NII, and retail distribution. The Demand Thesis product surfaces cohort-level QIB demand signals before mandate signing. Issuers get a data-driven view of which institutional cohorts are likely to participate and which are structurally excluded (such as ESG-constrained funds in regulated sectors) before a single intermediary is engaged.

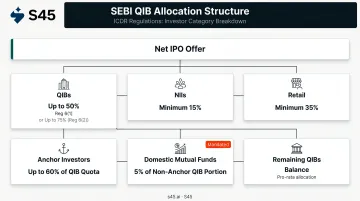

QIB Allocation Rules Under SEBI

The Two Allocation Routes

SEBI ICDR 2018 establishes two primary frameworks for QIB allocation:

- Regulation 6(1) — Standard route: Up to 50% of the net offer is allocated to QIBs, with at least 15% to NIIs and at least 35% to retail investors.

- Regulation 6(2) — Track-record gap route: Issuers that do not meet the standard eligibility conditions must allocate at least 75% of the net offer to QIBs. If that minimum QIB allotment is not achieved, the issue proceeds must be refunded.

The higher QIB requirement under Regulation 6(2) exists for a specific reason: loss-making or early-stage issuers carry more risk, and SEBI requires proportionately heavier institutional scrutiny before retail capital is exposed. For these issuers, the QIB book is a regulatory success condition — not just a credibility signal.

SEBI's 2025 board materials also reference a proposal to increase the QIB quota for IPOs exceeding ₹5,000 crore from 50% to 60%, with a corresponding reduction in the retail quota from 35% to 25%.

Internal Structure of the QIB Quota

Within the QIB portion itself:

- Up to 60% can be allocated to anchor investors

- 5% of the QIB portion (excluding anchors) is mandatorily reserved for domestic mutual funds

The mutual fund sub-quota reflects a policy rationale: mutual funds represent millions of retail SIP investors, so ensuring their participation in large public offerings serves a broad public interest.

Anchor Investors: A Closer Look

Anchor investors are QIBs that apply one day before the IPO opens, with a minimum application size of ₹10 crore. Their allocation is disclosed publicly before the IPO opens to all investors.

Lock-in structure:

- 50% of anchor allotment locked in for 30 days post-allotment

- Remaining 50% locked in for 90 days post-allotment

This staggered lock-in reduces early selling pressure, though the expiry dates create predictable supply events that issuers should plan around.

For IPOs above ₹250 crore, SEBI has expanded anchor investor capacity, scaled to issue size. Key thresholds to know:

- At least 2 QIBs must receive allotment for issues up to ₹250 crore

- At least 5 QIBs for issues above ₹250 crore

- No single QIB can receive more than 50% of the total issue size

If the QIB Quota Is Not Filled

Under SEBI rules, unsubscribed portions in any category can be moved to another category. An unfilled QIB quota signals institutional discomfort with valuation, business quality, or market timing. Issuers facing this situation typically have three options: reconsider pricing, reduce the issue size, or withdraw the IPO. Retail demand alone rarely compensates for institutional disinterest.

What Strong QIB Subscription Signals — and Its Limits

What Oversubscription Indicates

Prime Database reported an average overall IPO subscription of 28x across mainboard IPOs in FY2025-26 — though no accepted source publishes a formal average QIB subscription multiple. The practical benchmark is contextual: compare QIB subscription levels to recent comparable issuers in the same sector and size range, not to a universal threshold.

What high QIB subscription does create is a self-reinforcing demand cycle. Strong institutional bidding generates media coverage, draws NII participation (which is often leveraged and price-sensitive), and increases retail interest. The momentum compounds.

The Limitations

QIB participation does not guarantee post-listing performance. Three specific limitations are worth noting:

- Some institutions participate as short-term positions, especially when grey market premiums are elevated. Their exit on listing day can create early volatility.

- Anchor lock-in expiry at 30 and 90 days creates predictable selling windows — investors should track these dates for holdings they care about.

- The subscription multiple alone does not reveal book quality. A QIB register dominated by hedge funds and arbitrageurs looks identical in subscription data to one dominated by long-only funds with genuine conviction.

The Issuer Perspective

These limitations point directly to what issuers control: the quality of preparation going in. A company with clean financial disclosures, a coherent growth narrative, realistic pricing, and an experienced investment bank running the institutional roadshow is more likely to attract long-only QIB participation over short-term arbitrage capital.

Rushed or opaque IPO processes tend to produce weaker institutional books — even when headline subscription numbers look large. Strong demand volume is easier to generate than strong demand quality. The two are not the same thing.

Frequently Asked Questions

Who is eligible to be a QIB in an IPO?

Under Regulation 2(1)(ss) of SEBI ICDR Regulations 2018, eligible QIBs include mutual funds, scheduled commercial banks, IRDAI-registered insurers, FPIs (excluding individuals and family offices), AIFs, provident and pension funds with a minimum ₹25 crore corpus, public financial institutions, and systemically important NBFCs. Promoters and merchant bankers tied to the issue are explicitly excluded.

What is the role of QIB in an IPO?

QIBs serve three core functions in an IPO. Their large-ticket bookbuilding bids anchor price discovery, establishing where institutional demand sits. Strong QIB participation also signals credibility to retail and NII investors, and their 50% quota ensures the issuer raises the full targeted amount reliably.

What is the difference between NII and QIB in an IPO?

QIBs are SEBI-registered institutions allocated up to 50% of the issue with proportionate allotment. NIIs are HNIs and non-institutional applicants bidding above ₹2 lakh, allocated at least 15% — split between sNII (₹2–10 lakh) and bNII (above ₹10 lakh). Neither category can withdraw bids after the IPO closes. Unlike QIBs and retail investors, NIIs cannot bid at the cut-off price.

How much QIB subscription is considered good in an IPO?

Any subscription above 1x means the QIB quota is filled — that is the minimum threshold. Strong mainboard IPOs typically see QIB portions subscribed well above this, though no single universal benchmark applies. Context matters: compare against recent comparable IPOs in the same sector. Undersubscription in the QIB portion is a significant red flag regardless of other categories.

What happens if the QIB portion is not fully subscribed?

SEBI rules permit unsubscribed shares to be reallocated to other categories. In practice, an unfilled QIB portion signals institutional discomfort that retail demand alone cannot overcome — it typically leads to pricing revision, issue size reduction, or IPO withdrawal. Institutional disinterest is difficult to paper over with retail numbers.